In the spring of 2019, the government announced two changes for first time home buyers. The first time home buyer incentive and the change to the first time home buyer plan.

The home buyer incentive is a government program offered through CMHC where you will receive an incentive equal to 5% (for re-sale homes) or 10% (for new homes) of your home's purchase price. The money is provided interest free. Repayment is required at time of sale, calculated by multiplying fair market value by the percentage of the original incentive.

Buyers who receive the incentive are participating in a shared equity program with the government, through CMHC. There are a number of stipulations and different scenarios.

Calculate how much incentive that you could qualify! Scroll to the bottom of this article to use our calculator.

Let's review the guidelines, the pros and cons and look at some examples.

What are the requirements of the first time home buyer incentive?

- The first time home buyer must have the minimum 5% down payment to participate

- The maximum qualifying income is $120,000. That is, an individual purchasing can only earn a max of $120,000. A couple purchasing can have a combined income no more than $120,000.

- The maximum mortgage amount can not exceed four-times your qualifying income.

- The purchaser must be a first time home buyer. That is, in a four year period, you did not occupy a home that you or your spouse or common-law partner owned. Note, you can find the government definition of a first-time home buyer here.

- 5% Incentive is available for re-sale home purchase

- 10% incentive is available for new construction home purchase

- The incentive has a maximum term of 25 years. That is, it must be paid in full after 25 years, if the home isn't sold within that time.

- You must repay the incentive if you sell the home. This is calculated by multiplying the home's market value at time of sale (also known as the sale price) by the original incentive (5% or 10%).

- You have the choice to repay the incentive at any time prior to the sale of your home, if you wish. The calculation would be based on the market value of your home multiplied by the original incentive (5% or 10%).

- Standard mortgage qualifying criteria will apply. You must have adequate credit and confirm-able income to qualify for the mortgage.

What are the pros and cons of the first time home buyer incentive?

There are 3 advantages (pros) of utilizing the home buyer incentive.

- You owe less on your mortgage and therefore your payments will be lower

- You pay a lower CMHC insurance premium when you participate in the home buyer incentive program.

- If your home goes down in value, then the amount of money you must pay back to the government, when you sell, is less than what you received (although, if your home goes down in value, that's a con...)

There is 1 disadvantage (con) of utilizing the home buyer incentive.

- The government will receive more money if your home goes up in value when you sell.

How do you qualify for the 10% incentive?

To quality to receive 10% home buyer incentive, you must purchase a new construction home. You could choose to purchase a new single-family home or duplex. You could purchase a new townhouse or condominium. All of these would qualify for the 10% incentive.

If you purchased a new mobile home or manufactured home, then the maximum incentive is 5% of the purchase price.

When you purchase an existing home, town-home, condo, mobile home or manufactured home, then the maximum incentive is equal to 5% of the purchase price.

How do you pay back the first time home buyer incentive?

When I speak with clients, this part seems to create the most confusion. Let's look at this requirement from 3 perspectives.

- You live in your home for 25 years

- You sell your home

- You choose to pay back the home buyer incentive before you sell your home.

You live in your home for 25 years

The home buyer incentive has a term of 25 years. If you do not sell you home, then after 25 years you are required to pay back the incentive. There will be a market value assessment and you will be charged either 5% or 10% of that value, depending on what you received.

Let's assume you purchased a home for $400,000 and received a 5% incentive equal to $20,000.

After 25 years, if it's determined that your home is worth $800,000, then you would pay back 5% of that amount or $40,000

If after 25 years, it's determined that your home is worth $300,000, then you would pay back 5% of that amount or $15,000.

You sell your home

If you sell your home at any time prior to the end of the 25 year term, then the incentive becomes due in full.

The government would determine the market value of your home, typically the same as the sale price, and money would be directed to CMHC on the sale date.

The calculation would be the same as I did earlier.

Let's assume you purchased for $400,000 and received a 10% incentive or $40,000. If you sold the home for $600,000, then $60,000 (5% of the sale price) would be returned to the government on the sale date.

You may have noticed that I used "market value" of your home. I believe that the government is using this terminology to ensure there is no funny business with the sale price.

You choose to pay back the home buyer incentive before you sell your home

I can only think of a couple of situations where you might consider paying back the home buyer incentive early.

If you pay off your mortgage early and you want to get additional financing, then you may want to pay off the home buyer incentive. It appears that you don't have to pay back the home buyer incentive if you refinance your home, but it may be beneficial depending on what you are doing.

Connect with a mortgage broker to review your options. Try out our calculator below, then connect with us.

If you were planning major renovations, you might want to pay back the incentive early. Any improvements to your home at your expense will likely increase the value of your home. If you invest $50,000 or $100,000 or more on a renovation and your home goes up in value by that amount (or more), then you will owe a percentage of that gain to the government.

In this situation, I would pay off the incentive before starting any major renovations.

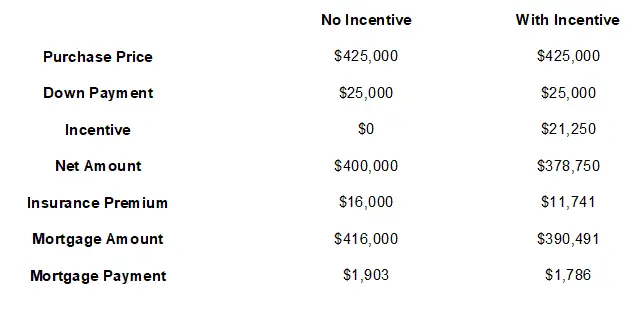

First Time Home Buyer Incentive Program for $100,000 Income Earner

Let's look at an example of a single purchaser (or a couple) with qualifying income of $100,000. Let's assume these buyers has saved $25,000 for the down payment. We can compare the payments and mortgage with and without an incentive.

Two advantages become obvious here. First, the default insurance premium is lower by $4,259. That's a win!

The second advantage is the payment is lower by $116.89 per month. I'm using an interest rate of 2.69% in this calculation.

Note: Rates could be higher or lower when you read this article. The main point is that there will be a savings regardless of the interest rate used! Another win!

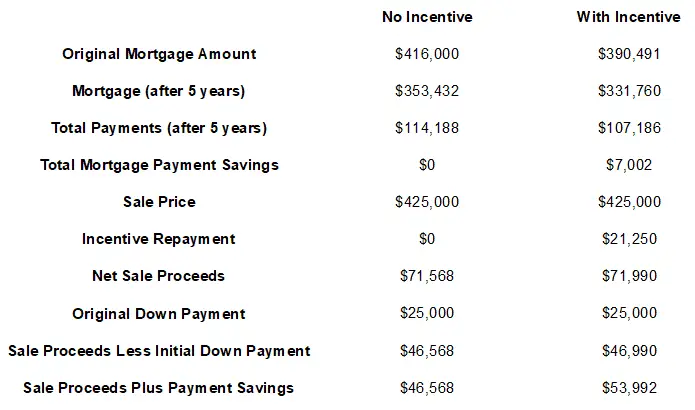

If after 5 years, this first time home buyer decided to sell the home. Let's assume the home doesn't increase in value, and is sold for $425,000. Let's also assume that the payments are kept the same over 5 years.

Then what? Let's look!

As you can see from the chart, above, the bulk of the savings comes from the reduced monthly payments. There is a reduce mortgage balance, but the starting mortgage balance was lower.

This home seller receives almost the same amount of money after selling the home, that is $71,568 versus $71,990. Factoring in the original down payment of $25,000, there is $46,568 versus $46,990 equity taken out.

From this comparison, I would conclude that the main benefit of choosing the home buyer incentive is the monthly payment savings. Over time this adds up.

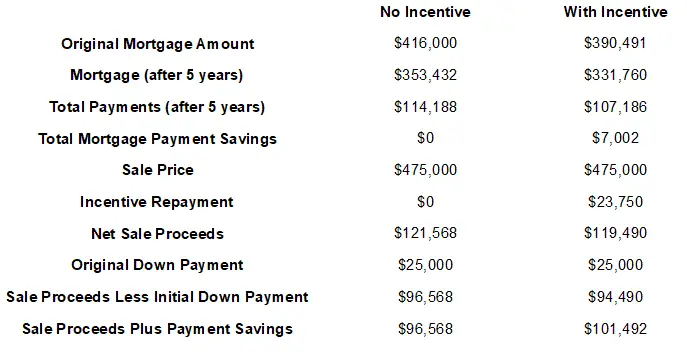

What if the home goes up in value after 5 years? Let's assume the home is sold for $475,000. Here are the numbers:

In this case, the overall benefit is lowered because the incentive repayment is higher than the original incentive received. There is still a monthly benefit no matter the sale price.

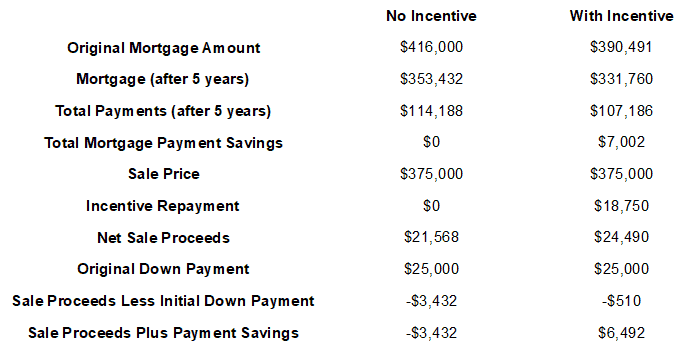

What if the home value drops by $50,000? Let's see what happens if the home is sold for $375,000. Here are the numbers:

As you can see from the results, if the home value drops, the incentive repayment also drops. Therefore, there is a still a net benefit by choosing the home buyer incentive.

No one wants their home to lose value. Choosing the first time home buyer incentive will provide you with a little bit of a hedge against values going down. You will also receive the monthly payment savings.

I've reviewed the 5% incentive. We could also go through the numbers with the 10% incentive, but they are very similar. The main benefit is the reduced payment amount.

Do you know your credit score? Check your credit online before you speak with someone.

If you want to calculate your maximum purchase price, you can use our tool below...

First Time Home Buyer Incentive: Calculate How Much You Qualify for

We created this calculator to help you figure out how much incentive you could potentially receive and what your maximum purchase price is based on your income. Enter the following info:

- Enter your annual income.

- Enter that amount of down payment, 5% if the minimum.

- Enter the interest rate. Connect with us through Facebook Messenger to get current rates.

- Enter the amortization, most first time home buyers choose 25 years.

Conclusion

If you are a first time home buyer and you meet the criteria to qualify for the incentive, then take advantage of it. There appears to be enough benefit to take advantage of the first time home buyer incentive program. You also get a slight hedge in the event home prices decline.

The main criteria to remember is as follows:

- Your qualifying income can not exceed $120,000 per year.

- Your total mortgage can not exceed four times your qualifying income.

- You must contribute a minimum of 5% toward the purchase

- You must qualify as a first time home buyer.

- The incentive is repaid at time of sale or 25 years, which ever comes first.

Would you choose to participate in the first time home buyer incentive program if you qualified? Let me know.

You can also watch our YouTube Channel for a quick review of the home buyer program.

Related Articles

What Is a Mortgage Pre-Approval?

Mortgage Pre-Approval Calculator, How Much Do You Qualify for?

What Do You Need For A Mortgage Pre-Approval

How Long Does It Take For Mortgage Pre-Approval?

How much mortgage do I qualify for?

How much income do I need to qualify for a mortgage?

How much down payment do I need to buy a home?

Can I qualify for a mortgage while on maternity leave?