As I write this article in the spring of 2020 I realize that we are living in history. Experts and scholars will be talking about, studying and evaluating the 2020 COVID-19 Pandemic for years and decades to come. But, I wanted to cover the options and choices that you have today?

If you own a home and have a mortgage, then you may be worried about making the payments. Even if your income hasn't been affected yet, you may want to cut your expenses so that you could afford your payments on a reduced income.

Let's review your options based on two scenarios:

- Your income has been reduced because of the pandemic

- Your income hasn't been affected yet, but you want to prepare.

If you prefer, I have created a video that you can watch that reviews your options and discusses what it looks like to have your mortgage payments deferred.

Let's review each of these in turn...

1. Your income has been reduced because of the COVID-19 Pandemic

If you or a member of your family has been affected by the COVID-19 virus, then you will have options to defer your mortgage payments with your lender. Every mortgage lender in Canada has been receiving thousands of calls daily with requests defer mortgage payments. Each lender has a slightly different process.

Payment deferrals could be for 1 month up to 6 months. Every lender is different, and it’s important to reach out to your own bank (monoline lender), trust company or credit union, depending on who you hold your mortgage with. I have a list of the phone numbers for these lenders at the bottom of this article.

How do you get the deferral?

Each lender is offering a different solution, so I would suggest that your first option should be to visit their website. Log in if you have access to do that and see if you can get a mortgage deferral without having to speak with anyone.

The phone lines are very busy, if you can get the next payment deferred, then you have time until your next payment to schedule an appointment or call when the phone lines are less busy. As mentioned earlier, I will provide a list of most lender's phone numbers for your reference, at the bottom of this article.

When calling, the phone lines are very busy so I would recommend that you call later in the day or the evening, when fewer people are calling. Your lender is likely prioritizing requests based on the coming payment date.

How will a payment deferral affect me?

When you defer a mortgage payment (also called skip a payment), the interest that would have been due for that payment is added to the principal of your mortgage.

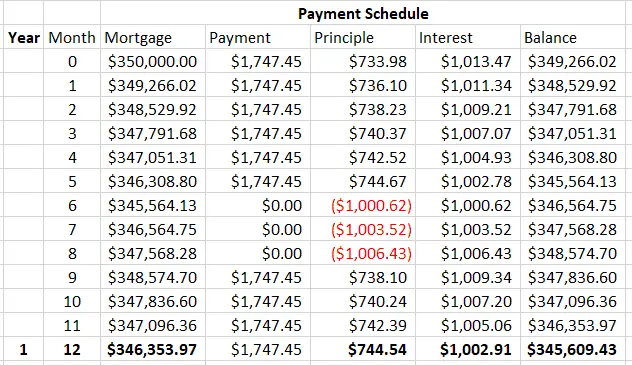

For example, let's say your regular monthly payment is $1750 and the interest portion of that payment is $1,000. If you defer the payment, then your mortgage balance will go up by $1,000 and you will pay interest on that until you make extra lump-sum payments up to $1,000 (plus interest) to pay that off.

If your interest rate is 3.5%, then that $1,000 of payment deferral will cost you approximately $35 per year (compounding). If you have 20 years remaining on your mortgage, then that 1 deferred payment will cost approximately $1,000 of extra interest (because of compounding).

This image shows 3 deferred payments. You can see that the principal of the mortgage increases by approximately $1,000 each month that the payment is deferred. In those months, you are not paying down the principal and the balance of the mortgage is increasing.

When the payment is deferred, the interest is added to that mortgage balance and the principal payment isn’t made. This means that to pay off the interest that’s deferred, you have to pay back that $1,000 plus the principal payment you didn’t make. This means that the interest compounding is slightly more than $35 per deferred payment per year.

Again, the video explains this fairly clearly.

Let’s look at options if your income wasn’t affected by the COVID-19 Pandemic.

Your income hasn't been affected yet, but you want to prepare.

If you are still working, or if you are still receiving the same income but want to put yourself in a better financial position to weather potential future issues, then you have a couple of options.

Consider Lowering Your Mortgage Payments

For must of us, our mortgage is our largest monthly expense. There are different ways to reduce that monthly expense.

Check Your Interest Rate

First, you could renew or switch to a lower interest rate. What interest rate is your mortgage at right now? Compare your interest rate to the mortgage rates available to you today.

If your interest rate is higher than what’s available, then you may be able to lower your interest rate and therefore your payments by switching to a lower rate. A lower interest rate could save you hundreds per month in mortgage payments and thousands over time in overall interest costs.

For example, A client of mine set up his mortgage in 2019. The best rate at that time was 3.89%, he set up this mortgage 14 months ago with an original term of 60 months. Last week, we secured an interest rate under 2.79% for him. Over the next 8 months, he will recover the penalty (which most of it was incorporated into the new mortgage) and his payments have reduced by more than $350 per month.

For this type of situation, it's important to look at your costs and the penalty to make sure you will recover your costs. I have a calculator that you can use to do that., find it here in this article: Why Should You Refinance Your Home

Check Your Amortization

Many clients have been paying slightly more than the minimum payment every month. You may have accelerated your mortgage payments in the past, by increasing by a few dollars to hundreds of dollars. If that’s the case, then your mortgage could be on schedule to be paid in less time than the original amortization.

Many lenders will allow you to bring your mortgage back to the original amortization by reducing the mortgage payment. You would have to speak with your specific lender about this.

Consider a Home Equity Line of Credit

If you already have a great rate or if the penalty to break the mortgage and to set up a new one is too big, then another option would be to set up a Home Equity Line Of Credit.

You may be able to set up a Home Equity Line of Credit (HELOC) so that you have access to some of the equity in your home. Home Equity Lines of Credit will typically offer lower interest rates than personal lines of credit or personal loans.

A HELOC is a fantastic financial tool that you can use to manage your money and provide access to the equity that is typically locked away in your home. It’s important that you have the discipline to use this tool wisely.

If you are considering a HELOC, you should watch this video about cash flow.

You don’t want to suddenly have access to $100,000 or more without a little bit of discipline or you may find that you’ve used it all up buying stuff!

By setting up the HELOC, you will have access to cash at better rates so that you can supplement your income if it's affected in the future.

Refinance your mortgage to consolidate debt

If you have credit card debt, lines of credit and personal loans. It may be worth it to refinance your mortgage (and pay the penalty, if there is one) to bring all your payments into one. Mortgage interest rates are at historic lows and consolidating debt could help you to reduce your monthly costs and improve your cash flow so that you can weather a financial storm.

Whenever you do a debt consolidation loan, I highly recommend that you also review your cash flow. To make a consolidation effective it's important to review your spending habits.

I posted a video on YouTube that talks about the advantages of refinancing and options between taking a loan or mortgage refinance to consolidate debt.

Watch that video here.

Summary

In these unprecedented times, it's important to be cautious with your health and your finances. These options provided in this article can help you with your mortgage finances.

As promised, here is the list of lenders and their phone numbers.

- ATB 1-800-332-8383

- B2B 1 800 263 8349

- BMO 1-877-895-3278

- Bridgewater 1-866-243-4301

- CIBC 1-800-465-2422

- CMLS 1-888-995-2657

- Optimum 1-866-441-3775

- Equitable 1-888-334-3313

- Connect First 403-736-4000

- Chinook Financial 403-934-3358

- First Calgary Financial 403-736-4000

- First National 1-888-488-0794

- Haventree 1-855-272-0051

- Home Trust 1-855-270-3630

- HSBC 1-888-310-4722

- ICICI 1-888-424-2422

- Manulife 1-877-765-2265

- MCAP 1-800-265-2624

- Merix 1-877-637-4911

- Marathon 1-855-503-6060

- National Bank 1-877-281-0144

- RBC 1-866-809-5800

- RFA 1-877-416-7873

- RMG 1-866-809-5800

- Scotia 1-800-472-6842

- Servus 1-877-378-8728

- Street Capital 1-866-683-8090

- TD 1-866-222-3456

- ATB 1-800-332-8383

- Servus CU 1-877-378-8728

If you aren’t sure what’s best for you, feel free to reach out to me. I’m happy to review your options and help you decide what’s best for you and your family.